Before the Funnel

Where B2B shortlists form, why most companies show up too late, and what to do about it.

Recently, I built a Claude agent to track and log B2B marketing research as it gets published. The first run was a sweep of the past 12 months: reports from Forrester, 6sense, Ahrefs, G2, Edelman, SparkToro, Stacker, Conductor, and many others. Luckily, none of the individual findings were new to me; I’ve been tracking this space closely enough that most of them landed as confirmation rather than discovery.

What was different (and an opportunity) was seeing all of it at once, in the context of each other and as a collective. And within that body of insights, one thing (unfortunately) stood out: B2B companies are still hung up on the old marketing/sales funnel and ignoring the realities of the buyers’ journey. And AI is only increasing the gap between how B2B companies are marketing and how B2B buyers actually buy.

What the buying journey actually looks like

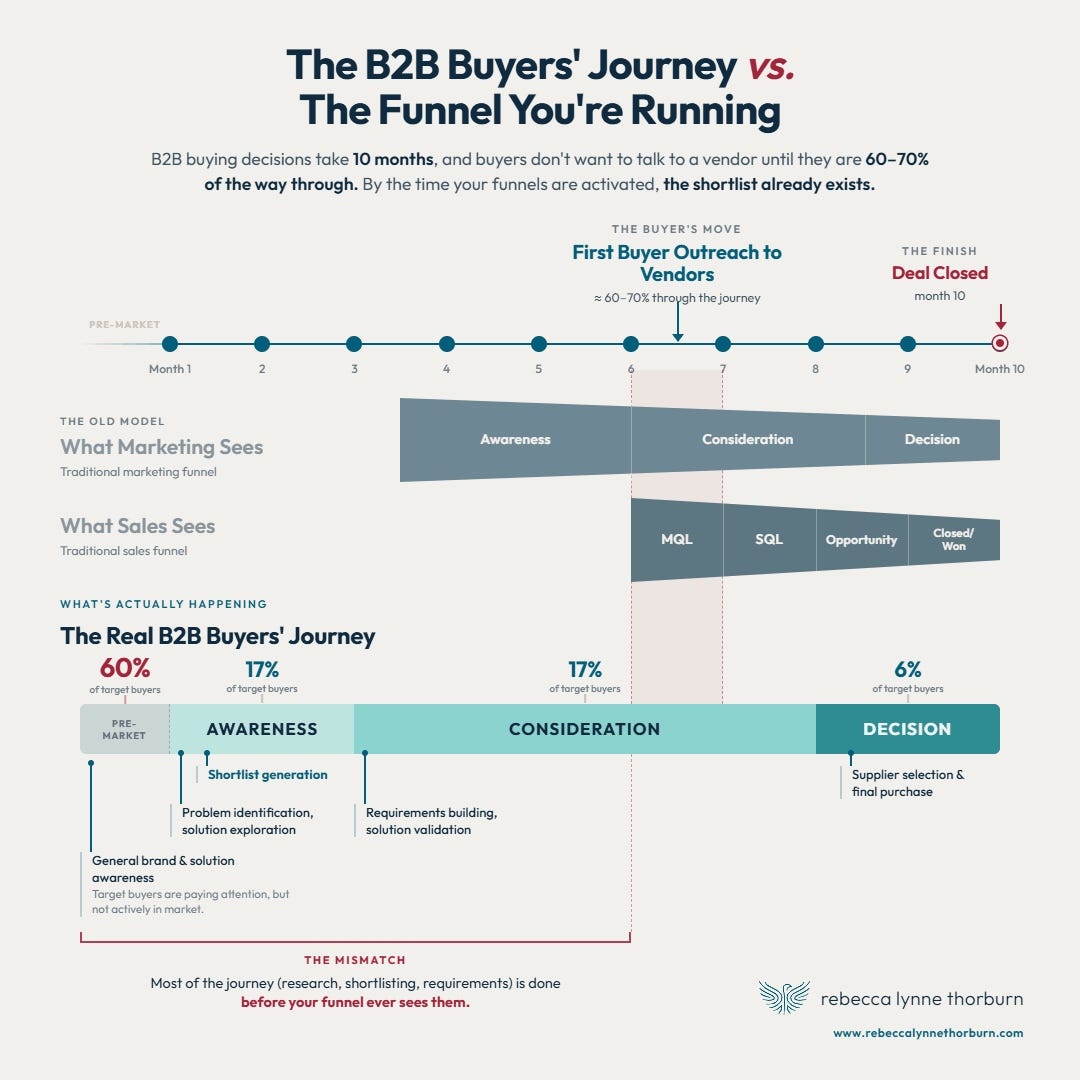

The research on this has been consistent for years, and the data continues to compound. The average B2B buying cycle runs about 10 months. Buyers don’t engage vendors until they’re 60–70% through that process — at which point they’ve established and initially vetted a shortlist, set requirements, and in 94% of cases, identified a preliminary winner.

This isn’t new data. 6sense has been publishing variations of this research for several years. Forrester’s 2026 buyer study corroborates it. And both sets of research tell us the impact of AI: over 90% of B2B buyers are using AI as part of their buying process, and buyers now rate AI as twice as meaningful a research source as vendor websites, product experts, or sales reps combined. Buyers delay contact until they’re deep into their own process, and in more than 80% of cases, they initiate that contact themselves.

The buying journey is about the buyer experience and perspective, not the vendor’s.

A B2B buying decision doesn’t begin when a buyer raises their hand. It starts when they recognize a problem worth solving. By the time anyone in that buying group has a meeting, starts an AI or Google search, or lands on a vendor’s website, they’re already well into a journey that typically runs 10 months from start to finish.

That journey has six recognizable phases, all necessary to align the buying committee and justify the decision:

Problem Identification — Can we clearly articulate and quantify the impact of this problem?

Solution Exploration — Do we understand what solutions exist, who’s providing them, and at what cost?

Requirements Building — What do we actually need? What are the must-haves versus nice-to-haves?

Solution Validation — Does this solution actually work for our organization?

Supplier Selection — Which vendor do we trust most? Do we have everything we need to choose?

Purchase — Can we secure budget, complete the process, and prepare for implementation?

The chart below maps all of this together: the six buyer phases set against both the traditional marketing funnel and the traditional sales funnel, layered with 6sense’s in-market math — showing what share of your target market is actively moving through each stage at any given moment, and when the traditional marketing and sales motions actually enter the picture. The overlap, or more precisely the lack of it, is the point.

The impact of this mismatch on B2B companies

Here’s the business consequence of ignoring this reality.

6sense’s 2026 State of the BDR, based on 872 respondents, found that the number one reason prospects say no is “wrong timing” — cited by 78% of BDRs operating without intent signal tools. Average quota attainment sits at 92%, statistically unchanged year over year. In that same period, average outreach volume has nearly doubled — from 17 touches per contact in 2024 to 34 in 2026. More effort. Same results.

The problem isn’t execution. It’s timing and visibility.

CommonMind’s 2026 survey of B2B SaaS marketers captures the awareness-to-action gap precisely: 93% say AI search visibility is critically important to their business. Only 14% have a mature strategy to address it. That gap — 93% awareness, 14% readiness — is not a technology problem. It’s a leadership problem.

2X’s 2026 AI Visibility Index found that 96% of B2B companies are invisible in the early-stage AI discovery process. My own research found that AI models describe the same brand in contradictory ways 28% of the time, and that the average B2B brand appears in fewer than 6 in 10 AI-generated responses in its category.

The in-market math makes the budget misallocation concrete. If only 17% of your ICP is in active consideration and 6% in decision at any given moment, and you’re concentrating the majority of your marketing investment on competing for that 2–6% in late-stage purchase, you’re writing off the 77% of your target buyers who are forming opinions right now about which vendors they’ll even consider when they are ready.

That’s the revenue problem no pipeline dashboard is showing you.

Why the wrong playbook keeps running

Before assigning blame, I want to clearly acknowledge that many marketing leaders already understand this. They’ve read the research. They know the funnel is an approximation of buyer behavior that broke sometime around 2012. The problem isn’t marketing’s understanding — it’s the organizational structures, tools, and executive mindsets that marketing has to work within.

CRM systems, marketing automation platforms, and attribution models are all built around funnel stages. The metrics marketing leaders report to CEOs and CFOs — MQLs, pipeline contribution, cost per lead — are funnel metrics. Changing what you measure means changing what you’re accountable for, which requires organizational trust that most marketing leaders can’t build while simultaneously hitting quarterly numbers.

Sales leaders who built their careers when sellers controlled information and outbound reliably created pipeline operate on a mental model genuinely at odds with how buyers behave now. The instinct to push harder on outbound when pipeline is soft is deeply ingrained — and the 6sense BDR data shows it happening in real time: outreach volume has nearly doubled in two years with no corresponding improvement in quota attainment.

The result is chronic overinvestment in the roughly 2-4% actively in late-stage purchase — the only segment that’s easy to measure — while the 77% forming opinions goes largely unaddressed, because there’s no CRM field for “paying attention but not yet buying.”

Now they’ve lost the last credible excuse.

In April 2026, Forrester — the analyst firm whose research justifies more B2B marketing budgets than any other — published “The GTM Singularity Is Here” at their annual B2B Summit. They weren’t hedging. Their language: B2B firms have failed to change how they engage with buyers, still clinging to MQL obsession, gated content, impersonal mass emailing, and siloed teams. Their VP of Research called it directly: “B2B leaders are facing a go-to-market crisis. The tried-and-true ways of creating demand, driving engagement, and understanding buyer intent can no longer keep pace with the changing buying landscape.”

When the firm your CEO and CFO trust to validate marketing investment publicly declares a go-to-market crisis, the “wait and see” posture has run out of runway.

Where AI actually fits

94% of buyers use AI as part of their purchasing process, per 6sense’s 2025 Buyer Experience Report. G2’s 2026 Answer Economy adds that 51% now begin their search in an AI chatbot specifically. And Forrester’s 2026 buyer study confirms that B2B buyers now rate AI as twice as meaningful a research source as vendor websites, product experts, or sales reps combined.

What we’re seeing is that AI is helping buyers compare vendor offerings, evaluate proposals, analyze internal stakeholder input, and summarize third-party content. AI is primarily a sorting and synthesizing tool — one that helps buying groups of 10 or more people, each with competing priorities, work through complexity and reach consensus.

LLM usage peaks mid-journey. 58% of buyers who used AI did so most intensively during the consideration phase — during solution validation and supplier selection — not at the top of the funnel. And buyers who used LLMs extensively engaged vendors later than those who didn’t (61% through the journey vs. 55%). AI made them more self-sufficient and more confident in their pre-contact conclusions.

AI isn’t building your shortlist from scratch. It confirms and refines a list that already exists — potentially adding a vendor that meets criteria buyers didn’t initially know to search for — then accelerates the vetting before anyone on the selling side knows a deal is in motion. And if AI can’t find consistent, accurate information about your brand, or the third-party validation buying groups need to build their internal business case, you don’t just lose the comparison round. You don’t survive the vetting phase.

To complicate things further, AI search results are…inconsistent. SparkToro’s research, based on 2,961 prompts across 600 volunteers on three platforms, found that asking an AI to recommend brands in a category 100 times produces the same list less than 1% of the time. AirOps’ 2026 State of AI Search found that only 30% of brands stay visible from one AI answer to the next. Semrush has named the phenomenon the “Mention-Source Divide”: fewer than 1 in 5 brands achieve both frequent mentions and consistent citations in AI answers.

Consistency of presence, not just presence, is the bar.

The practical implication: you can’t nurture your way onto a shortlist you were never on. Your content strategy needs a new primary question. Not “how do we get more traffic?”, rather “are we visible in the room where shortlists get built?”

Brand is the mechanism — and it works differently depending on your size

Brand isn’t a category separate from demand generation. It’s the mechanism by which companies get on — and survive — shortlists that form before any buying cycle is visible. But what that means in practice differs significantly depending on where your company sits.

The factors that drive AI citation are predominantly off-site. Ahrefs’ analysis of 75,000 brands found that branded web mentions correlate with AI Overview inclusion at 0.664, compared to 0.218 for backlinks — roughly three times more strongly. Stacker’s March 2026 research found that syndicated earned media produces a median 239% increase in AI citations compared to brand-owned content alone. Third-party mentions, analyst coverage, peer references, and earned media are what AI engines weight most heavily. Your owned content matters considerably less than what others publish about you.

Enterprise (1,000+ employees)

If you’re a known brand, you’re probably on more shortlists by default. The problem is mid-journey. AI is being used during solution validation and supplier selection to compare offerings, summarize third-party content, and help buying groups build their business case. If your narrative is fragmented — different positioning on your website versus review sites versus analyst coverage versus what customers say — you lose ground during exactly the phase where buying groups are working toward consensus.

My research found that brand authority and AI citation behavior don’t reliably track together. Being well-known and being accurately, consistently described by AI are not the same thing. For companies with broad portfolios, the challenge compounds: AI models frequently conflate individual solutions within a product family, describing them interchangeably or omitting them entirely. Visibility work at the corporate brand level often doesn’t transfer to specific solutions — each one may need its own structured presence. Audit what AI says about you across models — not just whether you appear, but whether the description is accurate. Rebalance budget away from late-stage Competitive Slice work toward the brand presence that shapes preference during solution exploration, months before buyers contact you.

Mid-market (100–1,000 employees)

You’re competing against enterprise incumbents who make shortlists by default and smaller challengers who move faster. Your category is probably established, but your representation in the third-party ecosystem AI draws from may be thin. When buying groups use AI to summarize third-party perspectives on vendors in your space, the question is whether your name appears consistently enough to survive the comparison round.

Invest in off-site presence before the next content calendar review — review platforms, trade publication coverage, industry analyst mentions. Structured comparison content (the “Top N” format) accounts for nearly 60% of AI-cited URLs according to GenOptima’s March 2026 analysis; standard blog posts and product pages are significantly underrepresented. Build competitor positioning pages that give AI accurate, brand-controlled information rather than leaving that gap for a competitor or a hallucination to fill.

Small business (10–200 employees)

You’re most likely missing shortlists before the vetting phase even starts. 2X’s data shows 96% of B2B companies invisible in early-stage AI discovery. My own research found 90% of B2B sites block AI agents at primary conversion points. When you do make a shortlist, AI-assisted vetting is how buyers check whether you can hold up against larger, better-known competitors — and a thin third-party ecosystem doesn’t survive that round well.

AI visibility is the genuine equalizer. Edelman’s research shows that 53% of B2B decision-makers say strong thought leadership makes brand recognition matter less. Third-party publishing, strategic review platform presence, and a narrative clear and specific enough for AI to summarize accurately are the levers. Check what AI currently says about you in your category. Most SMBs are surprised by what they find — or by what isn’t there at all. That’s where to start.

Getting leadership on board

This is where many marketing leaders are stuck. The data is clear, the case is made — but the CFO want to know why MQLs are down, the CRO wants to know why outbound is underperforming, and the CEO wants to know why sales cycles are longer.

Start with their language, not yours.

For the CFO, it’s an investment efficiency argument. Outreach volume doubled in two years with no corresponding improvement in quota attainment. That’s the clearest evidence the current approach is hitting diminishing returns. Reaching the 60% of your ICP currently in the problem identification and solution exploration phases costs a fraction per eventual deal compared to chasing the 2% in late-stage purchase — and shapes the criteria those buyers use before you ever have a chance to influence them.

For the CRO, it’s a timing argument. 78% of BDRs without signal tools cite “wrong timing” as the primary reason prospects say no. Those buyers aren’t saying no to your product — they’re saying no because the sales motion is hitting them at the wrong moment in a journey that started months earlier without you. More outreach doesn’t fix a timing problem. Visibility during solution exploration does.

For the CEO, it’s a competitive risk argument. 69% of buyers in G2’s 2026 survey chose a different software vendor than originally planned based on AI guidance. One in three bought from a company they had never heard of before the AI recommended it. The companies building AI visibility now are compounding structural advantages. The companies waiting are ceding shortlists they don’t know exist.

Forrester gives you the analyst cover to make all of it. “GTM singularity” is language your executives have seen from the firm they cite in board presentations. The market reality and the analyst validation are now aligned. The argument has never been better-supported — and the data has never been harder to ignore.

The question worth asking before the next planning cycle

If a buyer in your ICP asked an AI to help them compare vendors in your category today, would your solution appear? Would the description be accurate? Would it hold up during the mid-journey vetting phase, when buying committees are sorting through competing claims and working toward consensus before anyone picks up the phone?

Per the research, buyers are already doing exactly this — using AI to work through multi-stakeholder complexity in ways that happen entirely outside your line of sight.

The buyer’s journey didn’t get more complex. It got earlier, quieter, and more consequential before first contact. The funnel never captured that part of the decision. Adjusting for it now — before AI extends the invisible phase even further — is the work worth prioritizing.

If you’re still running the funnel while your buyers are building shortlists without you, that’s the problem worth solving first. I work with B2B technology companies on exactly this — AI visibility, strategic narrative, and GTM alignment. Let’s talk!